New Suit Update

In my recent post A New Suit I outlined three issues affecting precious metals prices that I didn’t think were getting the proper attention elsewhere. One of those issues was the way gold prices were moving inversely to oil prices. My thesis was that there was a tremendous amount oil short positions suffering margin calls or liquidation. This continued through last week. On Monday March 23 gold futures plunged from $4500 to $4100 and reversed, testing support at the 200 day moving average. Last Friday, March 27 gold and oil were both higher. So perhaps the liquidation there is nearly complete.

I am watching the US Treasury market this week for further confirmation. While the Bond Bogeymen are talking US bankruptcy, I believe, like gold, the backup in yields was liquidity driven. I’m watching the 4.50-4.60% level in the 10 year. This is a support level that has held since October 2023.

A second issue was futures pressure. Bullion banks trying desperately to have as many short positions as possible expire out of the money, was eliminated last Thursday as March futures expired. They managed to keep March futures just under $4500 at expiration.

I am still leery of Central Bank selling (or reduced purchasing) of gold and US Treasuries to pay oil bills and protect their own currencies. So I will be watching the US Dollar as weakness there would relieve at least part of the oil shock.

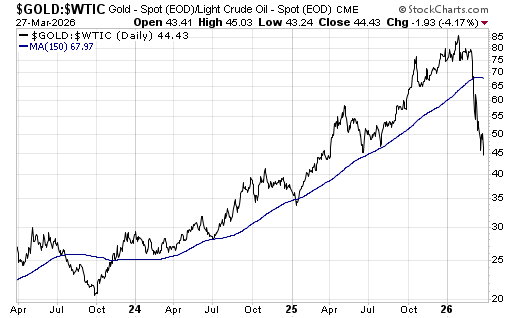

Gold equities continue to face headwinds. A positive gold/ oil has always influenced gold (and other miners) profit margins. This is not only because energy prices are a large input cost for miners, but because energy also influences many other input costs. The chart below shows that this ratio has collapsed. The gold/diesel chart would look even worse. At Dryden Gold, we have just been notified of 20% increases for drilling and lab costs. Large capital inflows into the mining space, over the past 6 months, is making drill rigs, with a crew, harder to find. Ramping up doesn’t happen overnight in an industry that has been capital starved for over a decade.

Gold prices averaged just under $4900 in Q1. Clearly, All In Sustaining Costs are rising. While many companies will report a blowout Q1, if metal prices move sideways coming out of this correction, Q1 might be their peak earnings for the rest of the year.